China’s Economy After Covid-19

- Gerard DiPippo

- Jun 8, 2023

- 19 min read

Updated: Aug 2, 2023

China's economy has emerged from "zero-Covid" without the inflation that occured in some other major economies but with reduced consumption, minimal private investment growth, a weakened real estate sector, high youth employment, and constrained local government finances. Beijing is banking on a surge of new household spending and is planning only marginal new stimulus measures. Chinese leaders, however, are sending contradictory signals to entrepreneurs and foreign investors. China will almost certainly achieve its conservative growth target of 5 percent this year. But in the next few years, Beijing's prioritization of national security over economic reforms will pose a risk to China's economic trajectory.

The Covid-19 pandemic presented the world with a natural experiment in which all economies and governments faced a similar shock. China’s experience of and economic policy responses to the pandemic were different from those of the other major economies, resulting in a different economic picture today. The United States and the other advanced economies provided massive additional fiscal and monetary support to their economies during 2020–22, whereas Beijing’s response was far more cautious and analogous to the stimulus policies it had already been relying upon for the past decade.[1] Much of the West endured waves of lockdowns (albeit of differing intensities), whereas China’s domestic economy remained basically open internally from mid-2020 until the Omicron-variant lockdowns of 2022.

The net effect at the macro level is that China’s gross domestic product (GDP) has recovered in real (inflation-adjusted) terms but remains below its pre-Covid trend in nominal terms. While economists typically talk about GDP growth in real (fixed price) terms, in the real world income, revenues, profits, debts, etc. exist as nominal values. This matters for the perceptions of businesses and households, and it is particularly relevant in a heavily indebted economy such as China’s. By the first quarter of 2023, China’s nominal GDP was about 2.6 percent below its trend in nominal terms, with an annualized GDP of 122 trillion yuan, or $17.9 trillion at market exchange rates (Figure 1). China’s inflation rate is within its historically normal range, unlike that in the United States and Europe, where inflation is high. In contrast, U.S. real GDP was about 2.6 percent below its pre-Covid trend, but nominal GDP – at $25.9 trillion – was about 5.8 percent above the pre-Covid trend because of high inflation.[2]

Sources: National Bureau of Statistics, author’s estimates.

As in other economies, China’s GDP growth fell dramatically at the beginning of the pandemic, but by late 2020 it had recovered. However, 2022 was a bad year for China’s economy because of the Omicron lockdowns, weakened property sector, and generally poor investor sentiment. In 2022, China reported real GDP growth of 3 percent, below Beijing’s target of 5.5 percent (Figure 2), with slower consumption and service-sector growth dragging down the overall economy. Some analysts suspect China’s true GDP growth was lower or even negative, especially given China’s implausible investment and consumption growth rates in the last quarter of 2022.[3] Whatever the number, China’s economy clearly weakened in 2022, which probably contributed to Beijing’s decision to abruptly abandon the “zero-Covid” policy in late 2022.[4]

Source: National Bureau of Statistics.

To assess where China’s economy stands and where it might be headed now that the country has reopened, it makes sense to consider the broad drivers behind its economic growth: consumption, investment, and net exports.[5] As shares of China’s overall economy (in nominal GDP, as of 2021), consumption – counting both households and the government – is the most important (54 percent), followed by investment (43 percent), and then net exports to the rest of the world (3 percent).[6] These drivers will be discussed in detail below in reverse order, from least to most likely to sustain China’s economic recovery.

The End of the Covid-19 Export Boom

The Covid-19 pandemic, although beginning in China, ended up benefiting China’s export sector. After the initial lockdowns in January and February 2020, Chinese factories quickly resumed normal production. As the rest of the world enacted public health measures and economic policies to mitigate the damage, demand for household goods, such as furniture, appliances, and electronics for telework and entertainment, soared. In U.S. dollar terms, China’s annualized goods exports went from about $2.5 trillion at the end of 2019 to $3.7 trillion by late 2022. Goods exports increased as a share of China’s nominal GDP from 17 percent in 2019 to 20 percent in late 2022.[7]

However, China’s economic gains from the surge in exports were nearly offset by the rise in global prices for many inputs, such as semiconductors. This is visible in the divergent growth rates for China’s exports and imports when calculated by value (U.S. dollar) terms versus by volume (tonnage) terms (Figure 3).

Source: General Administration of Customs.

China’s annualized goods trade surplus increased from $430 billion at the end of 2019 to $900 billion by late 2022.[8] In terms of GDP growth, this trade surplus is what counts. Net exports – including services, which were suppressed by travel restrictions – contributed 25 percent of China’s real GDP growth in 2020 and only slightly less than that in 2021–22. This was net exports’ largest contribution to China’s GDP growth since the late 1990s.[9] In that sense, the Covid-19 pandemic compelled China’s economy to revert to its older export-driven growth model.

But exports are unlikely to propel China’s economic growth going forward as global demand cools. The International Monetary Fund’s (IMF) April 2023 World Economic Outlook forecasts that global real GDP growth will slow from 3.4 percent in 2022 to 2.8 percent in 2023, with a more pronounced slowdown among the advanced economies that account for most of the demand for China’s exports.[10] Beijing is trying to support exporters with various measures, but such measures will at most only partially mitigate, not offset, the effects of slowing global demand.[11] This is not necessarily a problem, as it merely means reverting to the minimal or negative growth of China’s net exports prior to the pandemic. But it suggests that China will need to rely on domestic demand for growth, under its “dual circulation” strategy.[12]

Private-sector Investment is Lagging

China’s economy is more reliant on investment growth than are the other major economies because investment – and the domestic savings to fund it – accounts for a comparatively large share of its economy. China’s economy cannot fully recover unless investment recovers. Investment growth propped up China’s overall GDP growth last year, especially during the fourth quarter (Figure 2). Fixed asset investment grew only 5.1 percent in nominal terms last year, which is low by China’s standards.[13]

Most of that growth came from state-owned enterprises (SOEs). This tends to occur during periods of economic weakness, when the private sector pulls back and SOEs step up, including to fulfill their social stability functions. Last year, SOEs accounted for 38 percent of overall investment in terms of value but 71 percent of investment growth year on year (Figure 4).[14] Business sentiment among private firms has not yet recovered. Chinese private firms generally have less access to credit and instead they rely on retained earnings to fund investments. They will not resume investments unless they expect the economy to improve.

Sources: National Bureau of Statistics, author’s estimates.

Only cautious optimism about private investment is warranted. The National Bureau of Statistics (NBS) Purchasing Managers’ Index suggests that as of April manufacturers expected an improvement in production and business but were less hopeful than earlier in 2023.[15] The NBS also conducts surveys of businesses to estimate the Business Climate Index; this index suggests that business sentiment weakened in 2022, and as of the fourth quarter it was at its lowest level since the initial pandemic shock in early 2020.[16] The People’s Bank of China (PBOC) separately conducts surveys of industrial enterprises; that data suggest that industrial firms as of the first quarter of 2023 were more optimistic than they were in 2022, but nonetheless they expected business to contract.[17] The PBOC’s Banker Survey Index suggests a surge in demand for bank loans as of the first quarter of this year, which might indicate increased optimism.[18]

Sorting the fixed asset investment data by sector adds another layer to the story. Normally, the three largest contributors to investment are manufacturing (mostly private firms), infrastructure (mostly SOEs), and real estate (mixed). During 2018–19, as a pre-Covid baseline, manufacturing was 32 percent of fixed asset investment, real estate was 33 percent, and infrastructure was 22 percent. But in 2022 and early 2023, real estate investment declined along with the property sector (discussed below), dragging down growth of overall investment (Figure 5). Meanwhile, manufacturing investment was limited by slowing domestic and global demand, and infrastructure investment was constrained mostly by local government bond quotas and quasi-fiscal capacities linked to land sales. China’s investment growth will not recover to its pre-Covid rates unless the real estate sector recovers.

Sources: National Bureau of Statistics, author’s estimates.

The Decline of China’s Most Important Sector: Real Estate

China’s real estate and property sector is its most important sector for economic growth, investment, and financial and fiscal stability. The extent to which the dramatic slowdown in China’s property sector during the past two and a half years can be reversed is therefore likely to be a major determinant of China’s overall economic recovery. From 2018–2021, once all related inputs and sectors are included, China’s real estate and property sector accounted for about 25 percent of GDP, exceptionally high by international standards.[19] This is in part because of China’s rapid construction for urbanization and because Chinese households rely on real estate as an investment because of a lack of appealing alternative investments.

Beijing unveiled its “three red lines” policy in August 2020 to address property developers’ excessive borrowing and to tame China’s overheated real estate market.[20] Since 2016, President Xi Jinping has repeatedly said, “Houses are for living in, not for speculation.”[21] The policy was intended to push the property sector toward greater stability, but it pushed too hard, too fast, and in the middle of the pandemic. The result was a massive contraction – likely the largest in China’s history in absolute terms – in new construction and sales of new properties (Figure 6). In value terms, annualized residential property sales fell from a peak of 18 trillion yuan ($2.6 trillion) in mid-2021 to 11.7 trillion yuan ($1.7 trillion) by the end of 2022; the decrease is equivalent to 5 percent of China’s GDP in 2022.[22]

Sources: National Bureau of Statistics, author’s estimates.

By late 2021, Beijing had concluded its policies might have gone too far. Localities began loosening restrictions, and banks received guidance to help stabilize the property sector. By late 2022, Chinese banks had extended more than 3.19 trillion yuan ($460 billion) in lines of credit to property developers, which – if used – would increase real estate development loans by about 25 percent from their end-2022 level of 12.7 trillion yuan ($1.84 trillion).[23] This is separate from developers’ offshore bonds, which are the most salient default risk, with $141 billion of such bonds maturing in 2023.[24]

Another urgent issue for Beijing and localities is to make sure that property developers deliver the homes that have already been purchased.[25] One oddity of China’s real estate market is that most homes are purchased before they have been built, as normally purchasers are happy to buy investments in advance because of the high probability of appreciation. But even with the slowdown in purchases of new properties, this year 86 percent of sales were “in advance” as of April 2023.[26] From a financial perspective, a funding model where property developers can afford to finish previously sold properties only if they sell new properties in advance is, at least loosely, akin to a Ponzi scheme. The Chinese government is aware of this dynamic and of the risks of localized political instability if purchasers do not receive what they believe they were promised.[27] Therefore, the priority is stabilization, even if it means not quite solving the “speculation” problem that Xi has repeatedly identified.

The real estate sector as of early 2023 appeared to be turning around, albeit slowly. According to the NBS, as of April, 62 out of China’s top 70 cities registered month-on-month increases in the price of new residential properties. The uptick is most notable in Tier 3 and 4 cities, as these experienced the largest price declines after mid-2021; Tier 2 cities on average experienced flat, not falling prices, while prices in Tier 1 cities continued to rise.[28] The NBS reports that residential building sales increased by 12 percent in value terms but by only 3 percent in terms of floor space year on year during the first four months of 2023.[29]

Still, this year the real estate sector is unlikely to propel China’s growth even if it stabilizes. Indeed, some analysts argue that the true long-run demand for new housing based on demographic and urbanization factors, versus speculation, might be below the current levels of new construction.[30]

The Fiscal-Land Nexus and Constrained Local Government Finance

The property slowdown coincided with a reduction in land sales, which are important for local government finances. Gross government income from land sales (technically, land-usage rights, as the state owns all land in China) fell from 8.7 trillion yuan ($1.26 trillion) in 2021 to 6.7 trillion yuan ($969 billion) last year.[31] Property developers’ demand for new land fell with the demand for new houses (Figure 7).

Source: China Real Estate Information Website.

Land sales in China make local fiscal policy more pro-cyclical. When the economy – and the property sector – are hot, localities bring in more income from land sales. The gross values of land sales are large, but as sources of net revenues, they are generally only a modest contributor for local governments. This is because localities need to prepare the land for sale, including by compensating those being displaced. These expenditures nearly match the revenues from the sales. Consequently, net land sales were far smaller, equaling 951 billion yuan ($138 billion) in 2021 and 312 billion yuan ($45 billion) last year.[32] While a fall in land sales can constrain the localities’ resources for other purposes, a reduction in expenditures to prepare for the sales also means that total local fiscal expenditures fall as well. Land downturns become fiscal downturns, limiting fiscal spending when localities should be spending more to offset the economic effects of the downturn itself.

The property-land slowdown and net land-sales contraction were severe enough in 2022 to have major fiscal effects on localities. Last year was the first year in at least a decade that local fiscal resources from taxes, other revenues, and net land sales all declined (Figure 8). The central government increased its transfers to local governments for their main budgetary purposes by 18 percent, or 1.5 trillion yuan ($217 billion), last year, which nearly offset the lower gross revenues from land sales.[33] Nonetheless, governments were encouraged to “tighten their belts” to reduce expenditures, including by reducing civil servants’ benefits.[34]

Note: Including general and fund budgets.

Sources: National Bureau of Statistics, Ministry of Finance, author’s estimates.

The larger constraint on some localities is their decreasing ability to borrow more for off-balance sheet, or quasi-fiscal, spending via local government financing vehicles (LGFVs).[35] The IMF estimates that LGFV debts in 2022 increased by 14 percent to 57 trillion yuan ($8.3 trillion), or 47 percent of GDP (Figure 9).[36] Goldman Sachs has estimated that total LGFV debt was at 60 trillion yuan ($8.7 trillion) in 2022, with total central and local government debt – both official and implicit – at 152 trillion yuan ($22 trillion), or 126 percent of GDP, and more than 60 percent was owed by local governments.[37] Of course, LGFV repayment risks are not equally distributed across provinces.[38] In April, for example, Guizhou province sought assistance from a national asset management company (a distressed debt purchaser) to deal with its debts.[39]

Source: IMF Article IV reports.

Whatever the numbers, the bottom line is that some localities are nearing their maximum quasi-fiscal capacity, thus constraining their ability to enact new stimulus measures. Economic policymakers in Beijing were aware of this constraint when devising the plan for 2023.

The Plan for 2023: Households to the Rescue?

Beijing’s economic and fiscal targets for 2023 are conservative because the Chinese government is betting that reopening the economy after ending “zero-Covid” will do much of the work. The readout from the Central Economic Work Conference in December made it clear that boosting domestic demand through consumption would be the top priority this year.[40] At the National People’s Congress in March, Chinese leaders announced a real GDP growth target of “around 5 percent” for 2023.[41] This was on the low end of expectations, but it established an easily achievable target that will not require much incremental stimulus. Beijing also announced a quota of 3.8 trillion yuan ($550 billion) for special local government bond issuances, only slightly higher than that in 2022.[42]

The announced targets suggest that China’s consolidated on-budget deficit will reach 7.4 percent of GDP this year, up only slightly from last year (Figure 10). The fiscal impulse – the change in the fiscal deficit – is minimal, as Beijing is essentially trying to keep its fiscal powder dry due to local debt constraints and the need to preserve fiscal capacity for unforeseen shocks.

Sources: National Bureau of Statistics, Ministry of Finance, author’s estimates.

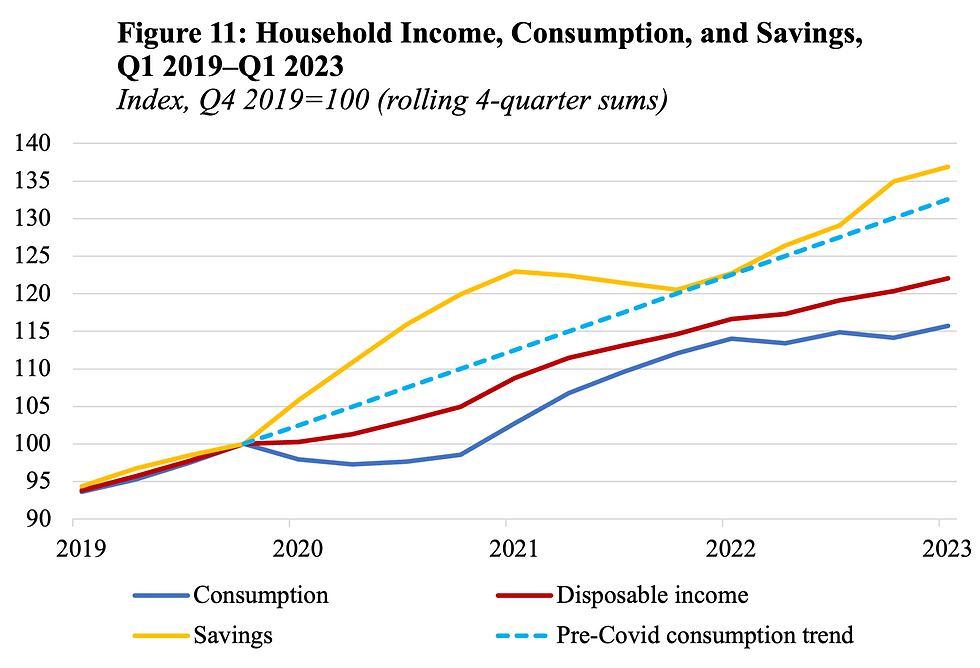

Households are expected to lead China’s economic recovery. Hopes hinge on assumptions about households’ desire to spend now that Covid-19 restrictions are gone. Chinese households on average have high savings rates, and their savings rates increased further during 2020–22 – to around 33 percent of disposable income – because of worries about their jobs and their inability to spend on services and travel. Household disposable income growth slowed markedly, but consumption slowed even more, pushing savings up (Figure 11).[43] Notably, the slowdown in income was the most dramatic for households with incomes in the lowest quintile, probably reflecting the weakened construction and services sectors.[44] Household borrowing slowed during 2022 because households were taking out fewer mortgages and saving more. Consequently, for the past two years household debt levels have been stable relative to GDP (68 percent) and household disposable income (115 percent).[45]

Household banking deposits have surged, but reported savings based on NBS surveys have not increased nearly as much. This suggests that the jump in savings deposits reflects mostly a reallocation of savings away from purchases of new properties amid the real estate slowdown.[46] Estimates of this “excess savings” range from 3–5 percent of China’s GDP.[47] Whatever the value, a strong consumption recovery depends on households wanting to spend down those balances.

Sources: National Bureau of Statistics, author’s estimates.

The consumption recovery is underway, but probably not as quickly as Beijing had hoped. In the first quarter of 2023, the services (tertiary) sector led real GDP growth, at 5.4 percent year on year. The hospitality and catering sector, which includes restaurants, jumped 13.6 percent.[48] Total consumption per capita and retail sales were up 5.4 percent and 5.8 percent, respectively, in nominal terms year on year.[49] Tourism and travel spending were strong during the Labor Day holiday.[50] However, monthly retail data from April disappointed market expectations.[51] The NBS Consumer Confidence Index indicates a collapse after February 2022, and Chinese consumers were only starting to recover as of March 2023.[52] The household savings rate during the first quarter of this year was nearly the same as that during the first quarters of 2021–22, which suggests that households are not spending down their “excessive savings.”[53]

Small and medium-sized enterprises (SMEs), especially in the services sector, are scarred by the effects of the lockdowns, but they might be the first to benefit from the consumption recovery. During 2020–22, SMEs received generous tax cuts as well as credit support from state banks. They were the primary beneficiaries of China’s tax cuts and rebates during the pandemic, which in 2022 totaled 4.2 trillion yuan ($610 billion).[54] This year, the Ministry of Finance expects tax and fee reductions of 1.2 trillion yuan ($173 billion), which will again benefit the SMEs.[55] From the end of 2019 through 2022, “financial inclusion” loans to small and individually owned enterprises grew from 11.6 trillion yuan ($1.7 trillion) to 23.8 trillion yuan ($3.4 trillion). The NBS does not report data that capture the SMEs’ balance sheets. Still, with annualized loan growth averaging 27 percent during a period when nominal GDP growth averaged 7 percent, we can assume that SMEs’ debts and repayment obligations increased much faster than their revenues.

Unemployment, especially among the young, is stubbornly high. This presents a bit of a chicken or egg problem, where more consumption is needed for job growth, but more income is needed to get consumption back to the pre-Covid trend. The employment components of the NBS Purchasing Managers’ Indexes for manufacturing and other sectors indicate that hiring contracted in both March and April.[56] The surveyed unemployment rate for urban Chinese ages 16–24 was above 20 percent in April, the highest on record in a series that goes back only through 2018.[57]

It is normal in many economies for younger workers to have higher unemployment rates, but in China’s case, the concern is the upward trend in the rate since 2020. A popular explanation is that Chinese universities are producing too many new graduates, with some more ridiculous claims that the problem is young workers’ unwillingness to do manual labor.[58] The more plausible explanation is that the sectors university graduates would normally go into – especially high-tech services – are doing poorly.[59] That is, it’s the economy. This debate is reminiscent of the “skills gap” arguments one heard in the United States after the Global Financial Crisis, which ended up disappearing as aggregate demand finally improved in the late 2010s.

Chinese leaders are understandably alarmed by this trend.[60] In April, the State Council announced a suite of measures to increase employment, especially among young graduates.[61] These measures include credit support to hiring firms, more hiring by SOEs and state or party entities, better training, and more assistance to the unemployed. Such measures might help but not as much as a broad-based macroeconomic recovery.

It is in this context that the Politburo met in late April to review the economy’s progress. Chinese leaders concluded that “demand is still insufficient” and they suggested that they would not tighten fiscal or monetary policy.[62] In practice, this means that government and infrastructure spending will probably be frontloaded this year. In the first quarter, local governments issued 1.32 trillion yuan ($191 billion) in special purpose bonds, 35 percent of the full-year quota.[63]

China’s fiscal policy remains focused on infrastructure, tax cuts, and targeted support, with little appetite for broad-based support for households. Chinese leaders are unlikely to deviate from their longstanding approach of supporting enterprises instead of supporting households. Beijing will continue subsidizing purchases of specific big-ticket items, such as electric vehicles and appliances.[64] However, households do not buy such durable goods often, so subsidizing their purchases today means pulling such sales forward from future years, at which point consumers will not need to buy them again. This is not a sustainable approach to consumption support. There is some discussion about increased support to low-income households – which spend a larger share of their additional earnings – through transfers via local governments but quantifying the extent of such support is difficult.[65]

Mixed Messages: Emphasizing National Security While Soothing Investors

Beijing’s efforts to heighten national security measures while also reassuring domestic and foreign investors to boost the recovery is a major tension in China’s current economic policy narrative. Xi has increased the salience of national security in economic policymaking because of fears about U.S. efforts to “contain” China’s economic and technological development. He has called for an acceleration of “self-reliance and self-strengthening in S&T and solving the problem of ‘strangleholds’ by foreign countries.”[66] In early March, Xi was explicit about his concerns: “…Western countries headed by the United States have contained, encircled, and suppressed China in an all-round way, bringing unprecedentedly severe challenges to China's development.”[67] At the National People’s Congress in March, he said, “We need to better coordinate development and security. Security is the foundation of development, and stability is the prerequisite for prosperity.”[68]

The party-state reforms announced in March reflect this prioritization of national security, and they reaffirm Beijing’s commitment to managing, if not resolving, financial risks.[69] The formation of the Central Science and Technology Commission and the reforms to the Ministry of Science and Technology are aimed at achieving self-reliance in key technologies to counter foreign “containment” risks.[70] The new Central Social Work Department has broad coordination responsibilities, including guiding private firms. The new State Administration of Financial Supervision (regulatory oversight), Central Financial Commission (policy guidance), and Central Financial Work Committee (ideological guidance) suggest that Xi was not satisfied with the previous arrangement, but it is not yet clear whether these new financial bodies mean that major policy changes are coming.

Other Chinese leaders are trying to reassure investors that China is fully reopened for business. In late March, Premier Li Qiang praised foreign investors at the China Development and Boao Forums.[71] The April Politburo meeting called for a “higher priority on attracting foreign investment.”[72] Chinese officials continue to emphasize the “two unwaverings,” with support for both SOEs and private firms making important contributions to the economy.[73] In late April, the meeting of the Central Commission for Comprehensively Deepening Reform highlighted the importance of supporting private enterprises.[74]

Foreign investor sentiment in China has soured since 2022, mostly because of the Covid-19 lockdowns, regulatory uncertainties, Beijing’s strategic support of Russia following its full-scale invasion of Ukraine, and cross-Strait tensions. Last year, foreign direct investment fell and foreign investors on net pulled money out of Chinese markets (Figure 12). Private equity investments in Greater China fell 53 percent year on year to $62 billion last year.[75] The annual China survey of the American Chamber of Commerce reflects increased pessimism about China as an investment destination.[76]

Note: Portfolio investment data for Q1 2023 unavailable as of time of publishing.

Source: State Administration of Foreign Exchange.

Recent actions by the Chinese authorities could undermine some of the enthusiasm following the reopening, and surely they are not helping to address foreign concerns. These actions include investigations of foreign due diligence, accounting, and consulting firms as well as the cybersecurity investigation into Micron Technology.[77] The authorities have also restricted overseas access to important economic and financial databases.[78] Chinese leaders may think they are sending a warning to the United States, but they are also alarming foreign firms. In late April, the U.S. Chamber of Commerce warned that investigations of U.S. firms and changes to the Counter Espionage Law are “dramatically” increasing the risks of doing business in China.[79]

What Comes Next?

China’s economy will almost certainly achieve Beijing’s real GDP growth target of 5 percent this year, at least according to the official data, barring any major shocks. The consumption recovery should continue for much of this year. But by late this year, a broader recovery, including from private investment, will be needed. It is not yet clear what can replace real estate, especially as a contributor to investment. The main contenders – manufacturing and infrastructure – will be limited by domestic or external demand and local government debt capacities, respectively. If consumption growth, which in nominal terms averaged 9 percent from 2017–2019 and was 5 percent as of the first quarter of this year, settles below its pre-Covid rate, China’s economic growth may be in for a structural downgrade.

Chinese leaders are sending contradictory signals to entrepreneurs and foreign investors at the same time that geopolitical tensions are rising. Few foreign firms that are invested in China will exit its large market entirely, but at the margins many are shifting investments to other destinations, often quietly.[80] China does not need foreign capital per se, but it still benefits from foreign technologies and competition. Actions that discourage foreign investment will affect China’s domestic market and investor sentiment more than its headline growth rate. Domestic investment is far more important for China’s economy, but Chinese private-sector entrepreneurs are not oblivious to the domestic regulatory or political environment, external demand signals, or geopolitical tensions.

A key risk is that Beijing’s worries about foreign “containment” efforts will reinforce the current national security bias over policies to support economic development and they will feed into Chinese leaders’ worst instincts about favoring control and stability. Xi’s statements suggest policies are heading in that direction, but economic policy in China is more reactive and less planned than many Western observers assume. Further foreign actions – especially by the United States – perceived as trying to stunt China’s modernization are far more likely to encourage party-state interventions than to encourage needed reforms. Geopolitical tensions will fuel Beijing’s fixation on indigenous technology, advanced manufacturing, and supply-chain security over productivity-enhanced reforms and service-sector development.[81]

China’s growth remains tied to the consumption of real goods and services, property cycles, and industrial production. The “new economy” – by the expansive NBS definition that includes the digital economy, new energy vehicles, other high-tech goods, healthcare, and other services – accounted for 17 percent of China’s value-added in 2021 and about 10 percent of its growth from 2019–21.[82] Despite much hype about emerging technologies and the “digital economy,” China’s economy is still primarily an “old economy.” In the next few years, measures that affect the entire economy will matter more for macroeconomic and financial stability and employment than efforts to lead in the supposed technologies of the future.[83]

About the Contributor

Gerard DiPippo is Senior Fellow in the Economics Program at the Center for Strategic and International Studies (CSIS). He joined CSIS after eleven years in the U.S. intelligence community (IC). From 2018 to 2021, DiPippo was Deputy National Intelligence Officer for Economic Issues at the National Intelligence Council, where he led the IC’s economic analysis of East Asia. He also was a senior economic analyst at the Central Intelligence Agency, focusing on East Asia, South Asia, and global economic issues. DiPippo holds a bachelor’s degree in economics and philosophy from Dartmouth College. His research focuses on Chinese economic issues, U.S.-China relations, sanctions, monetary and currency issues, and industrial policy.

Notes

[1] "Fiscal Monitor Database of Country Fiscal Measures in Response to the COVID-19 Pandemic," International Monetary Fund, October 2021. https://www.imf.org/en/Topics/imf-and-covid19/Fiscal-Policies-Database-in-Response-to-COVID-19. [2] “Bureau of Economic Analysis, GDP,” CEIC. https://www.ceicdata.com/en. [3] John Burn-Murdoch, "China’s GDP Blackout Isn’t Fooling Anyone," Financial Times, October 21, 2022. https://www.ft.com/content/43bea201-ff6c-4d94-8506-e58ff787802c; "BOFIT Forecast for China 2023–2025," Bank of Finland, April 20, 2023. https://www.bofit.fi/en/monitoring/forecasts-for-Russia-and-China/latest-forecast-for-china. [4] Lingling Wei and Jonathan Cheng, "Why Xi Jinping Reversed His Zero-Covid Policy in China," Wall Street Journal, January 4, 2023. https://www.wsj.com/articles/why-xi-jinping-reversed-his-zero-covid-policy-in-china-11672853171. [5] These are the components of GDP by the “expenditure method,” which is the international standard for calculating and presenting GDP. China’s National Bureau of Statistics, however, reports GDP primarily according to the “production method,” which estimates the value-added of different sectors, such as agriculture, manufacturing, and services. The two methods can be thought of as two sides of the same coin. [6] “National Bureau of Statistics, GDP by Expenditure,” CEIC. https://www.ceicdata.com/en. [7] “General Administration of Customs, China’s Goods Exports in RMB,” CEIC. https://www.ceicdata.com/en. [8] "Trade Balance, General Administration of Customs, Trade Balance," CEIC. https://www.ceicdata.com/en. [9] "National Bureau of Statistics, CN: Share to GDP Growth: Net Export of Goods and Services," CEIC. https://www.ceicdata.com/en. [10] World Economic Outlook: A Rocky Recovery (Washington, DC: International Monetary Fund, April 2023). https://www.imf.org/en/Publications/WEO/Issues/2023/04/11/world-economic-outlook-april-2023. [11] "国务院办公厅关于推动外贸: 稳规模优结构的意见” [Office of the State Council on Promoting Foreign Trade: Views on Stabilizing Scale and Optimizing Structure], Central Government of the People's Republic of China, April 11, 2023. http://www.gov.cn/zhengce/content/2023-04/25/content_5753130.htm. [12] He Lifeng, "高质量发展是全面建设社会主义现代化国家的首要任务” [High-quality Development Is the Most Important Task in Comprehensively Building a Socialist and Modernized Country], Central Government of the People's Republic of China, November 14, 2022. http://www.gov.cn/xinwen/2022-11/14/content_5726817.htm. [13] Fixed asset investment is investment in buildings, land, machinery, equipment, and infrastructure. Technically, the investment portion of GDP is called “gross capital formation,” which does not match “fixed asset investment” in part because the latter suffers from local overreporting and it counts land sales. However, the National Bureau of Statistics publishes gross capital formation data only annually and with a substantial lag. Therefore, analysts must rely on fixed asset investment for monthly or quarterly data. [14] The National Bureau of Statistics stopped reporting the yuan levels for most kinds of fixed asset investment after 2017. However, it is possible to estimate their subsequent levels, and therefore the shares of fixed asset investment growth, based on the reported growth rates of different types of investment applied to their earlier reported levels. [15] "National Bureau of Statistics, CN: PMI: Non Mfg: Business Expectation," CEIC. https://www.ceicdata.com/en. [16] "National Bureau of Statistics, CN: Business Climate Index (BCI)," CEIC. https://www.ceicdata.com/en. [17] "People’s Bank of China, CN: Diffusion Index: 5000 Industrial Enterprises Survey: General Business Condition," CEIC. https://www.ceicdata.com/en. [18] "People's Bank of China, CN: Banker Survey Index: Loan Demand," CEIC. https://www.ceicdata.com/en. [19] Kenneth S. Rogoff and Yuanchen Yang, "A Tale of Tier 3 Cities," Working Paper, National Bureau of Economic Research, September 2022. https://www.nber.org/papers/w30519. [20] "China May Ease 'Three Red Lines' Property Rules - Bloomberg News," Reuters, January 6, 2023. https://www.reuters.com/world/china/china-may-ease-three-red-lines-property-rules-bloomberg-news-2023-01-06/. [21] "Housing Should Be for Living In, Not for Speculation, Xi Says," Bloomberg, October 18, 2017. https://www.bloomberg.com/news/articles/2017-10-18/xi-renews-call-housing-should-be-for-living-in-not-speculation?sref=VZPf2pAM#xj4y7vzkg. [22] "National Bureau of Statistics, CN: Building Sold: ytd: Residential," CEIC. https://www.ceicdata.com/en. [23] Noriyuki Doi, "China Banks Throw $460bn Credit Lifeline to Real Estate Sector," Nikkei Asia, December 10, 2022. https://asia.nikkei.com/Business/Markets/China-debt-crunch/China-banks-throw-460bn-credit-lifeline-to-real-estate-sector. [24] Clare Jim, "China Developers' Debt Risks Persist After Support Policies' Slow Start," Reuters, January 17, 2023. https://www.reuters.com/markets/asia/china-developers-debt-risks-persist-after-support-policies-slow-start-2023-01-17/. [25] Isabelle Qian and Agnes Chang, "They Poured Their Savings Into Homes That Were Never Built," New York Times, January 24, 2023. https://www.nytimes.com/interactive/2023/01/24/world/asia/china-unfinished-apartments.html [26] "National Bureau of Statistics, CN: Floor Space Sold: ytd: Residential: Housing in Advance," CEIC. https://www.ceicdata.com/en. [27] Yuxiao Shan, "避免'房钱两空' 最高法新规明确购房者优先受偿” [To Avoid "Empty Houses and Money," New Regulations from the Supreme People's Court Clarify that Homebuyers Have Priority to Receive Compensation], Caixin, April 22, 2023. https://china.caixin.com/m/2023-04-22/102022542.html. [28] "National Bureau of Statistics, CN: Property Price Index: New Constructed: Commodity Residential by City, Grouped by City Tier," CEIC. https://www.ceicdata.com/en. [29] "National Bureau of Statistics, CN: Building Sold: YoY: ytd: Residential," CEIC. https://www.ceicdata.com/en; "National Bureau of Statistics, CN: Floor Space Sold: YoY: ytd: Residential," CEIC. https://www.ceicdata.com/en. [30] Logan Wright, Grasping Shadows: The Politics of China’s Deleveraging Campaign (Washington, DC: CSIS, April 2023), 69. https://www.csis.org/analysis/grasping-shadows-politics-chinas-deleveraging-campaign. [31] “Ministry of Finance, CN: Govt Revenue: Income from Land Usage Right Transfer,” CEIC. https://www.ceicdata.com/en. [32] Tom Hancock, “China’s Mysteriously Resilient Real Estate Prices—Explained," Bloomberg, March 25, 2023. https://www.bloomberg.com/news/newsletters/2023-03-25/china-s-mysteriously-resilient-real-estate-prices-new-economy-saturday?sref=VZPf2pAM. [33] "Ministry of Finance, CN: Govt Revenue: Local: Transfer from Central Govt," CEIC. https://www.ceicdata.com/en. [34] Keqiang Li, "Report on the Work of the Government Delivered at the First Session of the 14th National People’s Congress of the People’s Republic of China on March 5, 2023," NPC Observer, March 2023, 10. https://npcobserver.com/wp-content/uploads/2023/03/2023-Government-Work-Report.pdf; William Zheng, "China’s Civil Servants Ordered to Tighten Their Belts," South China Morning Post, January 12, 2022. https://www.scmp.com/news/china/politics/article/3162862/chinas-civil-servants-ordered-tighten-their-belts. [35] Nicholas Borst, "China’s Balance Sheet Challenge," China Leadership Monitor, March 1, 2023. https://www.prcleader.org/borst-spring-2023. [36] People's Republic of China, 2022 Article IV Consultation (Washington, DC: International Monetary Fund, February 2023). https://www.imf.org/en/Publications/CR/Issues/2023/02/02/Peoples-Republic-of-China-2022-Article-IV-Consultation-Press-Release-Staff-Report-and-529067. [37] Lisheng Wang et al., “The Size, Form and Implications of China’s Growing Government Debt,” Goldman Sachs Economic Research, April 2, 2023. [38] "China’s Debt Hangover," Macro Polo. https://macropolo.org/digital-projects/china-local-debt-hangover-map/ [39] "Editorial: Local Debt Discipline Cannot Be Relaxed," Caixin Global, April 24, 2023. https://www.caixinglobal.com/2023-04-24/editorial-local-debt-discipline-cannot-be-relaxed-102031500.html. [40] Xinhua, "China Holds Central Economic Work Conference to Plan for 2023," State Council of the People's Republic of China, December 17, 2022. https://english.www.gov.cn/news/topnews/202212/17/content_WS639d0051c6d0a757729e4885.html. [41] Li, "Report on the Work of the Government.” [42] Ministry of Finance, "Report on the Execution of the Central and Local Budgets for 2022 and on the Draft Central and Local Budgets for 2023,” NPC Observer, March 5, 2023. https://npcobserver.com/wp-content/uploads/2023/03/2023-MOF-Report.pdf. [43] "National Bureau of Statistics, “Disposable Income per Capita, Consumption Expenditure per Capita," CEIC. https://www.ceicdata.com/en. [44] "National Bureau of Statistics, Disposable Income per Capita by Income Level," CEIC. https://www.ceicdata.com/en. [45] "People's Bank of China, CN: Financial Inst: Local & Foreign Currency: Use: Loan: Domestic: Household," CEIC. https://www.ceicdata.com/en; "Center for National Balance Sheets, CN: National Balance Sheet: Household: Liability: Loan," CEIC. https://www.ceicdata.com/en; "National Bureau of Statistics, CN: Flow of Funds: Household: Source: Total Disposable Income," CEIC. https://www.ceicdata.com/en; "National Bureau of Statistics, GDP," CEIC. https://www.ceicdata.com/en. [46] As an economic accounting matter, property purchases count as investments, not consumption. Chinese households’ large savings are often funneled into new homes. Many economists have noted that China’s household consumption share of GDP is comparatively low. But this is a bit misleading because it reflects a strong preference for savings to buy new properties, which contribute to domestic demand and the real economy through construction and related inputs. [47] Stella Yifan Xie, "Covid-Era Savings Are Crucial to China’s Economic Recovery," Wall Street Journal, February 26, 2023. https://www.wsj.com/articles/covid-era-savings-are-crucial-to-chinas-economic-recovery-1ee3310b. [48] "National Bureau of Statistics, CN: GDP Index: YoY: Tertiary Industry (TI)," CEIC. https://www.ceicdata.com/en. [49] "National Bureau of Statistics, CN: Consumption Expenditure per Capita: ytd," CEIC. https://www.ceicdata.com/en; "National Bureau of Statistics, CN: Retail Sales of Consumer Goods: YoY: ytd," CEIC. https://www.ceicdata.com/en. [50] "China's consumer market sees booming sales on Labor Day," CGTN, May 3, 2023. https://news.cgtn.com/news/2023-05-03/China-s-consumer-market-sees-booming-sales-on-Labor-Day-1ju9k0YHYOc/index.html. [51] "China’s Waning Economic Recovery Spurs Calls for Stimulus," Bloomberg, May 15, 2023. https://www.bloomberg.com/news/articles/2023-05-16/china-s-economic-data-misses-forecasts-as-recovery-worries-mount?sref=VZPf2pAM#xj4y7vzkg. [52] "National Bureau of Statistics, CN: Consumer Confidence Index," CEIC. https://www.ceicdata.com/en. [53] "National Bureau of Statistics, Disposable Income per Capita, Consumption Expenditure per Capita," CEIC. https://www.ceicdata.com/en. [54] People's Daily, "去年新增减税降费及退税缓税缓费超4.2万亿” [Last Year, Newly Added Tax Cuts, Fee Reductions, Tax Refunds, and Tax Deferrals Exceeded 4.2 Trillion], Central Government of the People's Republic of China, February 3, 2023. http://www.gov.cn/xinwen/2023-02/03/content_5739811.htm. [55] Yanqiu Peng, "财政部:相关税费优惠政策预计全年可为经营主体减负约1.2万亿” [Ministry of Finance: Relevant Preferential Tax and Fee Policies Are Expected to Reduce the Burden on Business Entities by about 1.2 Trillion Yuan Throughout the Year], The Paper, April 18, 2023. https://m.thepaper.cn/newsDetail_forward_22749034. [56] "National Bureau of Statistics, CN: PMI: Manufacturing and Non-Manufacturing: Employment," CEIC. https://www.ceicdata.com/en. [57] "National Bureau of Statistics, CN: Surveyed Unemployment Rate: Urban: Ages 16 to 24," CEIC. https://www.ceicdata.com/en. [58] Sun Yu, "China Urges Jobless Graduates to ‘Roll Up Their Sleeves’ and Try Manual Work," Financial Times, April 22, 2023. https://www.ft.com/content/b0a85810-e8a2-4868-a88a-3049d54d101b. [59] "Editorial: Don’t Blame China’s Jobless Youth Problem on the Surge in New Graduates," Caixin Global, April 17, 2023. https://www.caixinglobal.com/2023-04-17/editorial-dont-blame-china-jobless-youth-problem-on-the-surge-in-new-graduates-102020548.html. [60] "Chinese vice premier stresses boosting employment for college graduates," Xinhua, May 11, 2023. https://english.news.cn/20230511/6ceb88dd71dc4b57915979f1db28067f/c.html. [61] "国务院办公厅关于优化调整稳就业政策措施: 全力促发展惠民生的通知” [General Office of the State Council on Optimizing and Adjusting Employment Stabilization Policies and Measures: Notice on Promoting Development and Benefiting the People's Livelihood], Central Government of the People's Republic of China, April 26, 2023. http://www.gov.cn/zhengce/content/2023-04/26/content_5753299.htm?mc_cid=b85b5d6087&mc_eid=227b82bd02. [62] "中共中央政治局召开会议 分析研究当前经济形势和经济工作” [The Politburo of the Central Committee of the Communist Party of China Holds a Meeting to Analyze and Study the Current Economic Situation and Economic Work], Central Government of the People's Republic of China, April 28, 2023. http://www.gov.cn/yaowen/2023-04/28/content_5753652.htm. [63] People's Daily Online, "一季度全国财政收入回稳向上 支出保持较高强度” [In the First Quarter, National Fiscal Revenue Stabilized and Expenditures Remained Relatively High], Ministry of Finance of the People's Republic of China, April 18, 2023. http://www.mof.gov.cn/zhengwuxinxi/caijingshidian/renminwang/202304/t20230418_3879558.htm?mc_cid=b79dc81624&mc_eid=227b82bd02. [64] "国家发展改革委4月新闻发布会 [National Development and Reform Commission April Press Conference], National Development and Reform Commission, April 18, 2023. https://www.ndrc.gov.cn/xwdt/wszb/gjfzggw4yxwfbh1/?mc_cid=955cd6c870&mc_eid=227b82bd02. [65] National Development and Reform Commission, "Report on the Implementation of the 2022 Plan for National Economic and Social Development and on the 2023 Draft Plan for National Economic and Social Development,” Wall Street Journal, March 5, 2023. https://s.wsj.net/public/resources/documents/2023CHINANPC_NDRC_EN.pdf. [66] People's Daily, "Xi Jinping Emphasizes the Need to Accelerate the Construction of the New Development Pattern and Enhance the Security Initiative in Development During the Second Collective Study Session of the Politburo of the CCP Central Committee," CSIS Interpret: China, January 31, 2023. https://interpret.csis.org/translations/xi-jinping-emphasizes-the-need-to-accelerate-the-construction-of-the-new-development-pattern-and-enhance-the-security-initiative-in-development-during-the-second-collective-study-session-of-the-politb/#:~:text=The%20second%20study%20session%20of,%2C%20and%20rural-urban%20divides. [67] "正确引导民营经济健康发展高质量发展” [Correctly Guide the Healthy Development of the Private Economy and High-quality Development], Xinhua Daily Telegraph, March 7, 2023. http://www.news.cn/mrdx/2023-03/07/c_1310701720.htm. [68] “(两会受权发布)习近平:在第十四届全国人民代表大会第一次会议上的讲话” [(Published under the Authority of the Two Sessions) Xi Jinping: Speech at the First Session of the Fourteenth National People's Congress], Xinhua, March 13, 2023. http://www.news.cn/politics/2023lh/2023-03/13/c_1129430112.htm. [69] "中共中央 国务院印发《党和国家机构改革方案》” [The Central Committee of the Communist Party of China and the State Council Issue the "Party and State Institutional Reform Plan"], Xinhua, March 16, 2023. http://www.news.cn/politics/zywj/2023-03/16/c_1129437368.htm?utm_source=substack&utm_medium=email. [70] "关于国务院机构改革方案的说明” [Explanation of the Institutional Reform Plan of the State Council], Central Government of the People's Republic of China, March 8, 2023. http://www.gov.cn/xinwen/2023-03/08/content_5745356.htm. [71] "Li Qiang Meets with International Delegates Attending the Annual Meeting of the China Development Forum 2023," Ministry of Foreign Affairs, March 28, 2023. https://www.fmprc.gov.cn/mfa_eng/wjdt_665385/wshd_665389/202303/t20230330_11051738.html; "China's Overtures to Foreign Firms Fall on Familiar Ears at 'Asia's Davos,'" Reuters, March 31, 2023. https://www.reuters.com/world/china/chinas-overtures-foreign-firms-fall-familiar-ears-asias-davos-2023-03-31/. [72] "中共中央政治局召开会议 分析研究当前经济形势和经济工作 中共中央总书记习近平主持会议” [The Politburo of the Central Committee of the Communist Party of China Holds a Meeting to Analyze and Study the Current Economic Situation and Economic Work. General Secretary of the Central Committee of the Communist Party of China Xi Jinping Presides Over the Meeting], Central Government of the People's Republic of China, April 28, 2023. http://www.gov.cn/yaowen/2023-04/28/content_5753652.htm. [73] People's Daily Online, "实现民营经济健康发展高质量发展(人民要论)”[Realize the Healthy Development of the Private Economy and High-quality Development (People's Theory)], April 18, 2023. http://paper.people.com.cn/rmrb/html/2023-04/18/nw.D110000renmrb_20230418_1-09.htm. [74] "习近平主持召开二十届中央全面深化改革委员会第一次会议强调 守正创新真抓实干 在新征程上谱写改革开放新篇章 李强王沪宁蔡奇出席” [Xi Jinping Presides Over the First Meeting of the 20th Central Committee for Comprehensively Deepening Reform, Emphasizing the Importance of Staying Upright and Innovating, Working Hard and Writing a New Chapter of Reform and Opening Up on the New Journey; Li Qiang, Wang Huning, and Cai Qi Attend], Xinhua, April 21, 2023. http://www.news.cn/politics/leaders/2023-04/21/c_1129548884.htm?mc_cid=0a498bf7c2&mc_eid=227b82bd02. [75] Gu Zhaowei, Guan Cong, and Han Wei, "China Private Equity Investment Plunges to Eight-Year Low," Caixin Global, April 19, 2023. https://www.caixinglobal.com/2023-04-19/china-private-equity-investment-plunges-to-eight-year-low-102021088.html. [76] Joyce Huang, "Survey: US Companies in China No Longer See It as Primary Investment Destination," Voice of America, March 3, 2023. https://www.voanews.com/a/survey-us-companies-in-china-no-longer-see-it-as-primary-investment-destination-/6987999.html. [77] Lingling Wei, "China Ratchets Up Pressure on Foreign Companies," Wall Street Journal, April 28, 2023. https://www.wsj.com/articles/china-ratchets-up-pressure-on-foreign-companies-524b958e. [78] Lingling Wei, Yoko Kubota, and Dan Strumpf, "China Locks Information on the Country Inside a Black Box," Wall Street Journal, April 30, 2023. https://www.wsj.com/articles/china-locks-information-on-the-country-inside-a-black-box-9c039928. [79] "U.S. Chamber Statement on Concerns Over PRC Investment Climate," U.S. Chamber of Commerce, April 28, 2023. https://www.uschamber.com/international/u-s-chamber-statement-on-concerns-over-prc-investment-climate. [80] Gerard DiPippo (contributor), "U.S.-China Trade Stayed Robust in 2022. Will That Last?" ChinaFile Conversation, February 28, 2023. https://www.chinafile.com/conversation/us-china-trade-stayed-robust-2022-will-last. [81] Innovative China: New Drivers of Growth (Washington, DC: World Bank Group, April 2019). https://documents1.worldbank.org/curated/en/833871568732137448/pdf/Innovative-China-New-Drivers-of-Growth.pdf; and "习近平主持召开二十届中央财经委员会第一次会议 [Xi Jinping presides over the first meeting of the 20th Central Financial and Economic Commission]," Central Government of the People's Republic of China, May 5, 2023. www.gov.cn/yaowen/2023-05/05/content_5754275.htm?mc_cid=9d3ee9f362&mc_eid=227b82bd02. [82] "National Bureau of Statistics, CN: Value Added of New Economy (New Industry, New Form and Model of Business)," CEIC. https://www.ceicdata.com/en; Betty Wang and Bansi Madhavani,

“China’s New Economy Brings Old Challenges,” ANZ Research, October 22, 2020. [83] Yiping Huang, "十三届全国人大常委会专题讲座第三十一讲” [Lecture 31 of the 13th National People's Congress Standing Committee Special Lectures], January 3, 2023. https://mp.weixin.qq.com/s/SOXuYFSnUdXwDG8cSwzmmw?mc_cid=27e24bb657&mc_eid=227b82bd02.

Photo credit: Wpcpey, CC BY-SA 4.0 <https://creativecommons.org/licenses/by-sa/4.0>, via Wikimedia Commons