What is Behind China's Dual Circulation Strategy

- Alicia Garcia Herrero

- Sep 1, 2021

- 16 min read

Dual circulation may sound like a buzzword without much relevance, but it is not. It actually enshrines China’s long-standing ambition to become self-sufficient. Such an ambition was made known to the world in 2015 after the launch of China’s industrial policy masterplan, Made in China 2025, even though the world at the time was still in full engagement with China. Since Trump’s push for a trade and technology war against China, the Chinese leadership has been relying on a dual circulation strategy to support China’s growth. This basically means insulating the domestic market from the rest of the world by eliminating any bottlenecks, whether in terms of natural resources or technology, so as to vertically integrate its production and achieve self-reliance served by China’s huge domestic market. A relevant consequence for the world, though, is that China will no longer need to import high-end inputs, with obvious negative consequences for major exporters of technology, such as Germany, Japan, South Korea, and the U.S. As if this were not enough, the second aspect of dual circulation, boosting external demand, in a context of Western containment, will increase the importance of the Belt and Road Initiative (BRI) to ensure open markets in the emerging world. In essence, dual circulation is part of China’s masterplan to become self-reliant in terms of resources and technology but also in terms of demand through its huge market as well as through third markets available through the BRI.

As has occurred with Chinese leaders in the past, key policy announcements are enshrined through the introduction of a short expression summarizing their intellectual underpinning. This tends to become a buzzword used to justify different policy actions, but they have large potential consequences in terms of China’s strategic direction. This has been the case for President Xi Jinping, after his landmark foreign policy strategy, namely the Belt and Road Initiative (一带一路) (BRI) launched in 2013 and his industrial policy strategy, Made in China 2025 (中国制造2025), and dual circulation (国内国际双循环) launched in 2020. The first time in which the concept of dual circulation was mentioned was May 14, 2020 in the midst of the protracted U.S.-China trade war, initiated by President Trump in early 2018, as well as in the midst of the Covid-19 pandemic. President Xi Jinping introduced the concept at a meeting of the Standing Committee of the Politburo, in a session devoted to containing the Covid-19 pandemic and improving the stability and competitiveness of Chinese industry.[1] Not many details were offered on this occasion, except for Xi’s brief clarification of the two dimensions of the concept, namely, internal circulation and external circulation, echoing the traditional two sources of aggregate demand – domestic demand and external demand. President Xi also mentioned that making full use of domestic resources to promote technological innovation was essential to ensuring China’s self-sufficiency in key areas. A further clarification of the concept came with President Xi’s August 20 speech to a group of social scientists,[2] when he noted two important factors relating to China’s growth pattern: first, the structural reduction in the current account surplus and the rising contribution of domestic demand, and, second, the role of supply reform to increase the contribution of domestic demand due to more value-added production. Similarly, in November 2020, China’s Vice Premier Liu He published a long article in the People’s Daily [3] to explain the “dual circulation framework,” with specific reference to the 14th Five-year Plan and China’s targets for 2035. Within this general objective, Liu He made six policy recommendations on implementation of the dual circulation strategy, with the last recommendation focusing on the need to open up. The other five recommendations were in line with President Xi’s quest for a strong domestic economy by promoting technological innovation, increasing domestic supply, improving financial services, increasing smarter urbanization, and boosting employment and income. Dual Circulation is Central to the 14th Five-year Plan The dual circulation strategy was crowned as a central part of China’s economic planning when the 14th Five-year Plan was unveiled during the Two Sessions (两会) beginning on March 4, 2021.[4] In fact, a full chapter (Chapter 4) of the Plan is dedicated to dual circulation,[5] but with more of a focus on “internal circulation” rather than external circulation, as a clear sign that self-reliance is an overriding objective. One notable aspect of how the dual circulation strategy in embedded in the Five-year Plan is the unification of domestic and foreign economic policies in one specific chapter. This differs from previous plans, in which economic strategies were more scattered, and it points to more coordination between domestic and external policies so as to achieve a single target, namely, self-reliance through technological upgrading. Second, covering both sources of growth jointly in a single chapter makes it even more clear that one can serve as a substitute — or a hedge — for the other. This is particularly important in the event of a shock, such as the Covid-19 pandemic, or a more structural change in the external environment, such as the radical change from engagement to containment in U.S. attitudes toward China. For many analysts, the dual circulation strategy is nothing more than a more sophisticated name for China’s policy response to the global financial crisis, i.e., a “rebalancing” away from the vanishing external demand to the internal market. This strategy became even more specific after the massive infrastructure-led investment boom financed by China’s 2008 fiscal stimulus. In fact, the concept of rebalancing referred to increasing reliance on domestic consumption rather than on exports or investment, and it became the mantra of a number of key economic policies, such as the massive push to increase wages so as to create room to boost household consumption. In the same vein, the dual circulation strategy was also announced only several months after a sudden external shock, namely the Covid-19 pandemic, so it might appear that these two strategies differ only in terms of their names, but this is not the case. There is actually an important difference between the two in terms of the external context. When China introduced its rebalancing strategy, the West, and particularly the U.S., was fully engaged with China and multilateralism was very much in vogue. In contrast, President Xi’s announcement of the dual circulation strategy came about after a protracted trade and technology war that President Trump started in early 2018. The policies introduced to contain China’s technological rise, such as the “entity list” forbidding exports of key inputs to some of China’s key technology companies, including 5G providers such as Huawei, clearly had a bearing in China’s much more aggressive push for the self-reliance enshrined in the dual circulation strategy. During the months between President Xi’s first mention of the new strategy to its inclusion in the 14th Five-year Plan, there were no signs of improvement in the external environment. The Biden administration has basically kept in place most of the China-related policies of the Trump era, including the various restrictions on technology transfers, whether through exports or Chinese acquisitions of overseas technology companies. Furthermore, the Biden administration has been much more proactive in seeking support from U.S. allies with respect to China. Against this backdrop, the response of Chinese policy-makers to the external risk, that is, self- reliance, has clearly not lost ground, and if anything, the opposite has occurred. The above does not really mean that the Chinese leadership’s quest for self-reliance would not have occurred without an external threat. In fact, a focus on technological development and industrial policy was present in previous five-year plans, but this has occurred in a much more aggressive way after President Xi came to power. The best example of China’s quest to move up the ladder in key strategic sectors through industrial policy is the Made in China 2025 program announced on May 8, 2015 by the State Council.[6] In fact, China’s catch-up with the developed world in terms of research and development expenditures has been astounding and China has thus increased its sophistication of production and exports (Figures 1 and 2).

The rebalancing mantra was really all about boosting domestic demand to mitigate the sharp fall in external demand, which ended in an investment boom—more than a huge increase in consumption—as household income until 2008 remained low and there had been meager growth during the previous five years. The focus on supply policies was still absent. It finally come about, with great fanfare, with China’s 2015 major industrial-policy tool—Made in China 2025. The rebalancing in 2008 also relied on raising the contribution of domestic demand to China's growth. It was coupled with the idea that driven by faster growth in domestic consumption, China's long-standing current account surplus would, as imports increased, give way to a deficit. This time, however, the notion is to ensure that more of that increased demand is met by domestic production rather than by imports. In this regard, the dual circulation strategy is a corollary of the government's previous Made in China 2025 program to upgrade China's technological capacity as it has become possible to substitute high-end goods only due to advances in key sectors. In fact, such an industrial policy tool incorporates setting targets for domestic sourcing of intermediate goods in key industries — from semiconductors to electric vehicles — leading to a reduction in China’s imports of such intermediate goods. Put another way, the previous rebalancing was about reducing China's dependence on exports. In contrast, the thrust of dual circulation is about reducing dependence on imports and increasing self-sufficiency. This can be equated with a "hedged integration" to protect the Chinese economy from volatility from abroad, while still benefiting from selling in overseas markets. How the Dual Circulation Strategy Is Being Implemented After the concept was launched and, even more so, after it appeared in the 14th Five-year Plan, a number of more specific policies have been developed by the National Development and Reform Commission (NDRC). The first, issued on September 9, 2020, aims to ease supply-side bottlenecks for production, under the lemma of “promoting deep integration and innovative development of the logistics and manufacturing industry.[7] The plan sets goals to reduce production and logistic costs and to improve the efficiency of distribution. The focus is not only the physical integration of manufacturing enterprises but also the enhancement of information-sharing through the use of 5G. This plan not only covers domestic logistics but also those for export markets. An important implication of the dual circulation strategy, and more generally of the 14th Five- year Plan, is the push for basic science. Indeed, unlike the previous plan for 2005–20, the “Medium and Long Term Plan for Science and Technology 2021–35” focuses on foundational technologies. In a related document, the NDRC reiterates support for priority sectors, including the next generation IT, biotech, high-end manufacturing, new materials, new energy, electric vehicles, environmental protection, and digital creativity.[8] The Ministry of Commerce (MOFCOM), in its own five-year plan, has started to use the concept of dual circulation to introduce measures supportive of domestic consumption and a diversification of trade. The best example of the former is new measures announced in February 2021 in the auto sector to stop local governments from introducing restrictions on car purchases, while requesting subsidies from them for the purchase of electric vehicles.[9] As for the latter, on March 1, 2021, MOFCOM announced measures to increase the presence of foreign investors at the highest end of China’s value chain,[10] aiming of course at further integrating vertically China’s production capacity. More recently, six ministries and government agencies jointly issued guiding opinions aimed at accelerating the development of small and medium-sized enterprises (SMEs) active in technologies listed in the Industrial Four Bases Development Catalogue (工业“四基”发展目录), a supplement to the Made in China 2025 Strategy (中国制造2025). The policy aims to cultivate SMEs into “little giant” companies that excel in niche sectors. Similarly, MOFCOM has also published a guideline for the diversification of imports in a way that reliance on the Western economies is reduced by giving more weight to emerging economies, especially the Russian economy.[11] Furthermore, MOFCOM, together with the Ministry of Industry and Information Technology (MIIT) and the Cyberspace Administration of China (CAC), have jointly issued a guideline to support the expansion of China’s digital economy internationally by setting up international R&D centers.[12] In sum, measures to support domestic demand and upgrade China’s supply chain through inward FDI or technological upgrading are all associated with the internal channel of the dual circulation strategy. In addition, attempts to diversify the sources of imports away from the developed economies, especially the U.S. or its close allies such as Australia, aim at boosting China’s own ecosystem and export markets, especially in the emerging world. This is, of course, supported by the improved logistical connectivity through BRI-related investments and also by the expansion of China’s digital commercial capabilities overseas. Potential Sectoral Impact The general objective of the dual circulation strategy, namely self-reliance, has important sectoral implications. The first is that the upgrading of China’s industrial power will reduce its dependence on the rest of the world and eliminate potential bottlenecks, which are often linked to either natural resources or technology. Regarding natural resources, the scarcity of energy and metals to meet its demand needs was formerly considered China’s Achilles Heel, but swift action has minimized this potential bottleneck. In fact, during the last few years, China has invested massive funds to the scarcity overcome the scarcity oil and metal resources, and also scarcities of lithium, cobalt, and rare earth metals, which are key to the new technologies. This explains not only the global buying spree by energy and mining companies but also the creation of new trading routes under the Belt and Road Strategy. Construction of the port of Guadar in Pakistan linked to the Mainland through the China-Pakistan Economic Corridor is a good example of a hedge against potential problems in the Strait of Hormuz or the Strait of Malacca. Beyond buying resources and building alternative routes, China also has committed heavy subsidies to make sure that its resource constraints do not hamper China’s external competitiveness. China’s energy sector, by far its most heavily subsidized, in particular, Petro China and SINOPEC that received the largest subsidies among Chinese listed companies in 2020.*Finally, beyond ensuring the provision of external resources and subsidizing their use, China is starting to protect domestic use of such resources in line with the dual circulation plan of placing a priority on support to the domestic economy. An important example is the recent elimination of the export tax rebate on iron ore, the price of which has been increasing aggressively of late.[13] The second target for China’s quest to achieve self-reliance is technology. China has clearly leapfrogged over many countries in terms of technological capacity by investing large sums in research and development (R&D). In fact, China’s average R&D expenditures as a percentage of GDP have already surpassed those of the EU, although they still remain lower than those in the U.S. In several sectors, for instance, 5G and Artificial Intelligence, China appears to be at the technological edge, but this is not the case for the key components that are required by most technologies, that is, semiconductors. This is clearly the most important bottleneck facing China’s self-reliance dream. Chinese imports of semiconductors are already greater than its oil imports (Figure 3) and they are actually the number-one item in China’s import basket. Furthermore, China is really behind in producing high-end semiconductors or in entering the highest end of the semiconductor supply chain. * Subsidies amounted to RMB 11 billion and RMB 8.7 billion respectively, according to their Financial statements (available in Wind).

This is why an upgrading of the semiconductor industry was one of the key objectives of Made in China 2025, accompanied by a dedicated RMB 140 billion fund—the National Integrated Circuit Industry Investment Fund, known as the Big Fund, that was introduced in 2014. Phase 2 of the Big Fund was introduced in 2019, with RMB 204 billion. Beyond these funds amounting to about USD 60 billion, other tax incentives and tax rebates have also been introduced in this sector. In order to support chip production, China will increase tax deductions, and, according to China Daily, [14] “for every 1 million yuan ($150,000) spent on R&D, a company will see 2 million yuan deducted from its taxable income.” Despite a strong policy push, the results seem limited so far. According to IC Insights, in 2020 China-headquartered companies only accounted for 5.9 percent of market share in the country’s total integrated circuit market. [15] The question remains whether all of the money spent to support China’s most important bottleneck to vertical integration will succeed. There are different opinions, but it remains an open question. What is certain is there have been louder voices calling for tougher export controls, investment screening, and the building of an alliance among like-minded countries, as noted by the United States–China Economic and Security Review Commission [16] and the Information Technology and Innovation Foundation. [17] This means China’s path toward self-reliance in chip-making will only become more difficult. The second aspect of dual circulation is about supporting domestic demand and, in particular, shifting toward a consumption-based growth model. This can be understood as renewed support for the new economy. In fact, the importance of the new economy has grown over the years, but the dual circulation strategy is bound to accelerate this process (Figure 4).

In fact, investments in new sectors have grown massively, especially in three key areas: the semiconductor, consumer, and health care sectors (Figure 5). Such an investment boom in the new sectors cannot be explained by their very high profitability, at least not when compared with their global peers (Figure 6).

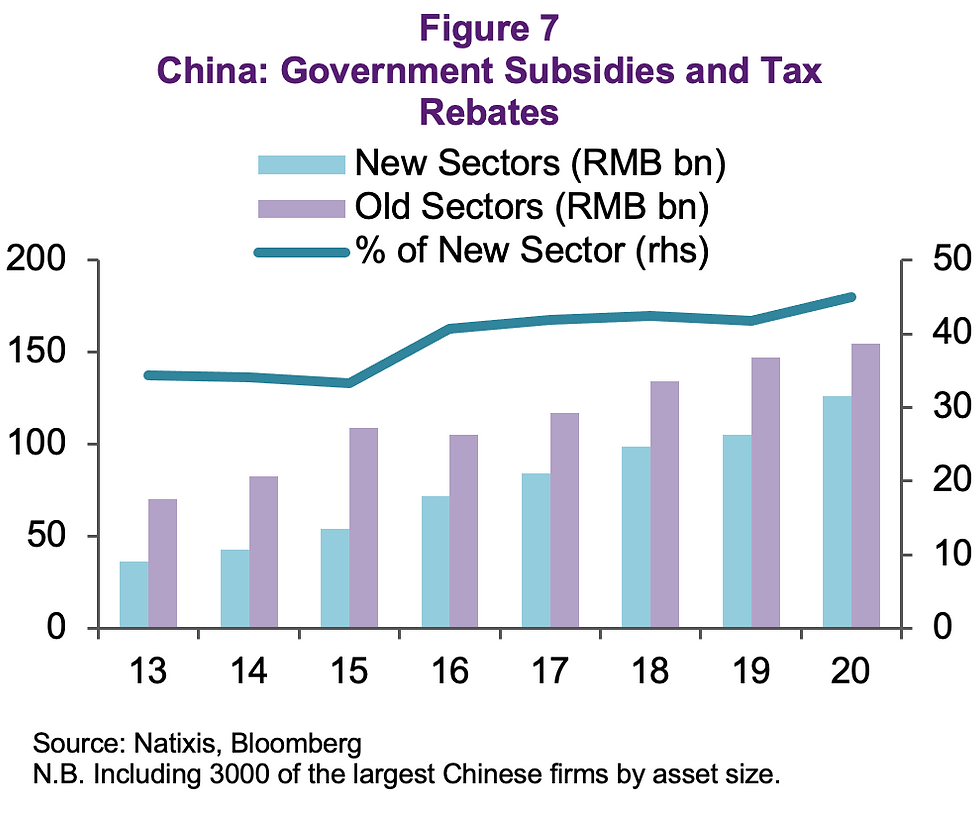

Massive government subsidies are probably a better explanation for such an investment boom. In fact, the share of direct government subsidies in the new economy has increased from 33 percent in 2015 to 45 percent in 2020, especially in the consumer sector but also in ICT. In contrast, subsidies to old sectors have been more volatile, although they still have been large in the energy sector and the industrial and material sectors.

What This Means for the Rest of the World The way the dual circulation strategy is interpreted, whether similar to the idea of rebalancing or as a quest for self-reliance, has major implications for the rest of the world. The rebalancing strategy in 2008 relied on raising the contribution of domestic demand to China's growth, but this was done with the support of imported goods. In fact, Chinese imports of commodities and intermediate goods ballooned beginning from 2008 as a consequence of China’s infra-led fiscal stimulus. The rebalancing mantra was coupled with the idea that faster growth of domestic consumption would result in a reduction of China’s longstanding current account surplus and that this was a natural course in the country’s development model. It was of course great news for the rest of the world as it boosted most countries' exports to China. Figure 10 shows that exports to China by the world’s major economies witnessed positive growth rates during the past decade.

In contrast, dual circulation is geared toward achieving self-reliance, or self-sufficiency. The implication is that imports can be substituted for domestic production as soon as China is able to produce them domestically. Moving to the terminology of supply chains, this is nothing but the vertical integration of manufacturing production within China rather than sourcing inputs from the rest of the world. In other words, China's foreign partners might see much less of an increase in exports to China, particularly high-end manufacturing equipment, than was the case after 2008 with the rebalancing strategy. This should be particularly problematic for Germany, Japan, and South Korea, but also for Taiwan and the U.S. as the main exporters of intermediate goods, whether machinery, chemicals, auto parts, or semiconductors, to the mainland. Furthermore, and in the best spirit of the dual circulation strategy, not only does China intend to substitute its imports as soon as it is capable of producing such intermediate goods,* but also it expects to export them, competing with these larger exporters in third markets. In fact, this is already occurring. China is already competing with Germany in key export sectors, such as autos, industrial and electrical machinery, and the same is true for Japan and the United States (Figure 11). *China’s export structure has become increasingly similar to that of the major exporters of high-end intermediate goods, such as the EU, the U.S. and also Korea and Japan.

In fact, third market competition is already a harsh reality for the most advanced exporters of manufacturing. Europe, for example, has lost market share in Russia [18] and Latin America,[19] for example, and this is bound to increase as China’s quest for technological upgrading results in more value-added sectors. In other words, the dual circulation strategy, rather than a manna from heaven for the rest of the world, might result in a double whammy, especially for exporters of high-end intermediate products. In some key sectors in the future (whether for energy sustainability or digitization), China has already leapfrogged past many of the incumbents. A good example is renewable energy, and especially solar panels, as China already counts for 71 percent of the global production share — from barely 15 percent in 2006 — while Japan and Germany, once the leaders, have clearly fallen behind (Figures 12–13).

Conclusion The dual circulation strategy might initially appear to be a buzzword, but it actually has very important implications both for China and the world. If we move beyond the obvious, namely, the boost in both domestic and external demand, the dual circulation strategy is really about self-reliance in response to a more hostile external environment. In other words, China is turning closer to an economic model on the import side, but not on the export side, as a way to ensure that China’s technological progress will be able to continue independently of U.S. intentions. An important and positive consequence of China’s moving up the ladder through a technological upgrading is that it will be able to dominate export markets in more sectors (particularly high-end sectors). This is very different from the old rebalancing strategy that Chinese policy-makers introduced in response beginning from to the global financial crisis. The push for a consumption-based model at that time represented a call for more, rather than fewer, imports, as is the case for the dual circulation strategy. One could argue that the rebalancing strategy was in line with China’s external environment at that time, namely, engagement with the superpower, the U.S. The dual circulation strategy is the result of China’s new “Weltanshau,” namely. a much more hostile world with the hegemon trying to contain China’s rise. It is important to note that China’s push for self-sufficiency is not only a problem for the rest of the world, particularly the major exporters of high-end goods, but also for China itself. The reason is that China’s own quest for decoupling will require huge financial resources, with all the related inefficiencies. The size of the inefficiencies will depend on how far China is from the technological frontiers and what China can do to shorten that distance. Acquisitions of foreign companies in areas where China suffers from the most important bottlenecks can clearly help, as in the case of semiconductors, but that route seems increasingly difficult as the developed economies step up scrutiny of Chinese acquisitions. As China continues to close its economy through the mantra of self-reliance, it will find it increasingly difficult to maintain a competitive edge. This could result in China eventually losing its international competitiveness. Within that context, China’s Belt and Road Strategy can be seen as an important complementary policy to the dual circulation policy. By building transport infrastructure in a hub-and-spoke mode, China is basically ensuring that economies linked through such an infrastructure will increasingly depend on China for imports. If the world ends up with two ecosystems, China will count as one, as it develops its technology to cover all its needs and as it develops its own standards, as conceived by China’s manufacturing 2035. In sum, the dual circulation strategy is a crucial policy that clearly reflects China’s view of the world and its place in it. China is seeking to become a fully integrated market with no need for help from the rest of the world, though still benefiting from export markets. If the U.S. pushes for decoupling and takes its allies along, China can always rely on its own allies along the Belt and Road. As regards global imbalances, the dual circulation strategy might result in another trade surplus for China as imports would be controlled so to reduce excessive dependence on the rest of the world, but exports will be further promoted as a way to monetize China’s efforts to move up the ladder. In other words, the new dual circulation policy can basically be understood as an important substitution strategy that keeps foreign markets open for Chinese goods. Therefore, the dual circulation strategy should not be dismissed as a buzzword. Rather, its implementation will entail major consequences.

About the Contributor

Alicia García Herrero is Adjunct Professor at Hong Kong University of Science and Technology and Senior Research Fellow at Bruegel (Brussels).

Notes

[1] “Xi Jinping Chairs the Meeting of Standing Committee of the Political Bureau of the CPC Central Committee,” Xinhua Net, May 14, 2020, http://www.xinhuanet.com/politics/leaders/2020-05/14/c_1125986000.htm (accessed August 10, 2021).

[2] “Xi Jinping’s Speech at the Symposium of Experts in Economic and Social Fields,” Xinhua Net, August 24, 2020, http://www.xinhuanet.com/politics/leaders/2020-08/24/c_1126407772.htm (accessed August 10, 2021).

[3] Liu He, “Accelerate the Construction of the New Development Pattern with Domestic Circulation as the Main Body and Domestic and International Dual Circulation Promoting Each Other (Studying and Implementing the Spirit of the Fifth Plenary Session of the 19th Central Committee of the Party),” People’s Daily, November 25, 2020, http://politics.people.com.cn/n1/2020/1125/c1001-31943814.html (accessed August 10, 2021).

[4] “The Fourteenth Five-Year Plan for National Economic and Social Development of the People's Republic of China and the Outline of the Long-term Goals for 2035,” National Development and Reform Commission, https://www.ndrc.gov.cn/xxgk/zcfb/ghwb/202103/P020210323538797779059.pdf (accessed August 10, 2021).

[5] Chapter 4 of “The Fourteenth Five-Year Plan for National Economic and Social Development of the People's Republic of China and the Outline of the Long-term Goals for 2035,” National Development and Reform Commission, https://www.ndrc.gov.cn/xxgk/zcfb/ghwb/202103/P020210323538797779059.pdf (accessed August 10, 2021).

[6] “Notice about Issuing ‘Made in China 2025,’” State Council, http://www.gov.cn/zhengce/content/2015-05/19/content_9784.htm (accessed August 10, 2021).

[7] “Plan to Promote Deep Integration and Innovative Development of the Logistics and Manufacturing Industry,” National Development and Reform Commission, https://www.ndrc.gov.cn/xxgk/zcfb/tz/202009/P020200909333031287206.pdf (accessed August 10, 2021).

[8] “Guiding Opinions on Expanding Investment in Strategic Emerging Industries, Cultivating and Growing New Growth Points and Growth Poles,” National Development and Reform Commission, https://www.ndrc.gov.cn/xxgk/zcfb/tz/202009/t20200925_1239582.html (accessed August 10, 2021).

[9] “The Ministry of Commerce Announces Several Policies to Streamline ‘Dual Circulation,’” Xinhua Net, February 10, 2021, http://www.xinhuanet.com/fortune/2021-02/10/c_1127089178.htm (accessed August 10, 2021).

[10] “The Ministry of Commerce Issues a Notice on Building a New Development Pattern and Stabilizing Foreign Investment,” Ministry of Commerce, http://www.mofcom.gov.cn/article/ae/ai/202103/20210303041579.shtml (in Chinese) (accessed August 10, 2021).

[11] “Notice of the Ministry of Commerce on Printing and Distributing the ‘Fourteenth Five-year Plan for Business Development’,” Ministry of Commerce, http://www.mofcom.gov.cn/article/guihua/202107/20210703174101.shtml (accessed August 10, 2021).

[12] “Guidelines for Outward Investment Cooperation in the Digital Economy,” Ministry of Industry and Information Technology and the Cyberspace Administration of China, http://images.mofcom.gov.cn/hzs/202107/20210723142119100.pdf (accessed August 10, 2021).

[13] “China Makes Policy Changes to Curtail Crude Steel Production: Beroe Inc.,” Cision, June 22, 2021, https://www.prnewswire.com/news-releases/china-makes-policy-changes-to-curtail-crude-steel-production-beroe-inc-301317109.html (accessed August 10, 2021).

[14] “More R&D Tax Incentives in Pipeline,” China Daily, March 25, 2021, http://global.chinadaily.com.cn/a/202103/25/WS605bd982a31024ad0bab16d2.html (accessed August 10, 2021).

[15] “Sales of Logic ICs Account for Largest Share of China’s IC Market in 2020,” IC Insights, https://www.icinsights.com/data/articles/documents/1347.pdf (accessed August 10, 2021).

[16] “Transcript of Hearing on China’s 13th Five-year Plan,” U.S.-China Economic and Security Review Commission, https://www.uscc.gov/sites/default/files/transcripts/April%2027,%202016%20Hearing%20Transcript_0.pdf (accessed August 10, 2021).

[17] “Moore’s Law Under Attack: The Impact of China’s Policies on Global Semiconductor Innovation,” Information Technology and Innovatoin Foundation, February 18, 2021, https://itif.org/publications/2021/02/18/moores-law-under-attack-impact-chinas-policies-global-semiconductor (accessed August 10, 2021).

[18] Alicia García-Herrero and Jianwei Xu, "The China-Russia Trade Relationship and its Impact on Europe," Working Paper (Bruegel), no. 4 (2016), https://www.bruegel.org/wp-content/uploads/2016/07/WP-2016_04-180716.pdf (accessed August 14, 2021)/

[19]Alicia García-Herrero, Thibault Marbach, and Jianwei Xu, "European and Chinese Trade Competition in Third Markets: The Case of Latin America," Working Paper (Bruegel), no. 6 (June 7,2018), https://www.bruegel.org/wp-content/uploads/2018/06/WP-2018-06_-060618.pdf (accessed August 14, 2021).

[20] “China's Solar Panel Makers Top Global Field But Challenges Loom,” Nikkei Asia, July 31, 2019, https://asia.nikkei.com/Business/Business-trends/China-s-solar-panel-makers-top-global-field-but-challenges-loom (accessed August 10, 2021).

Photo credit: AlfvanBeem, CC0, via Wikimedia Commons